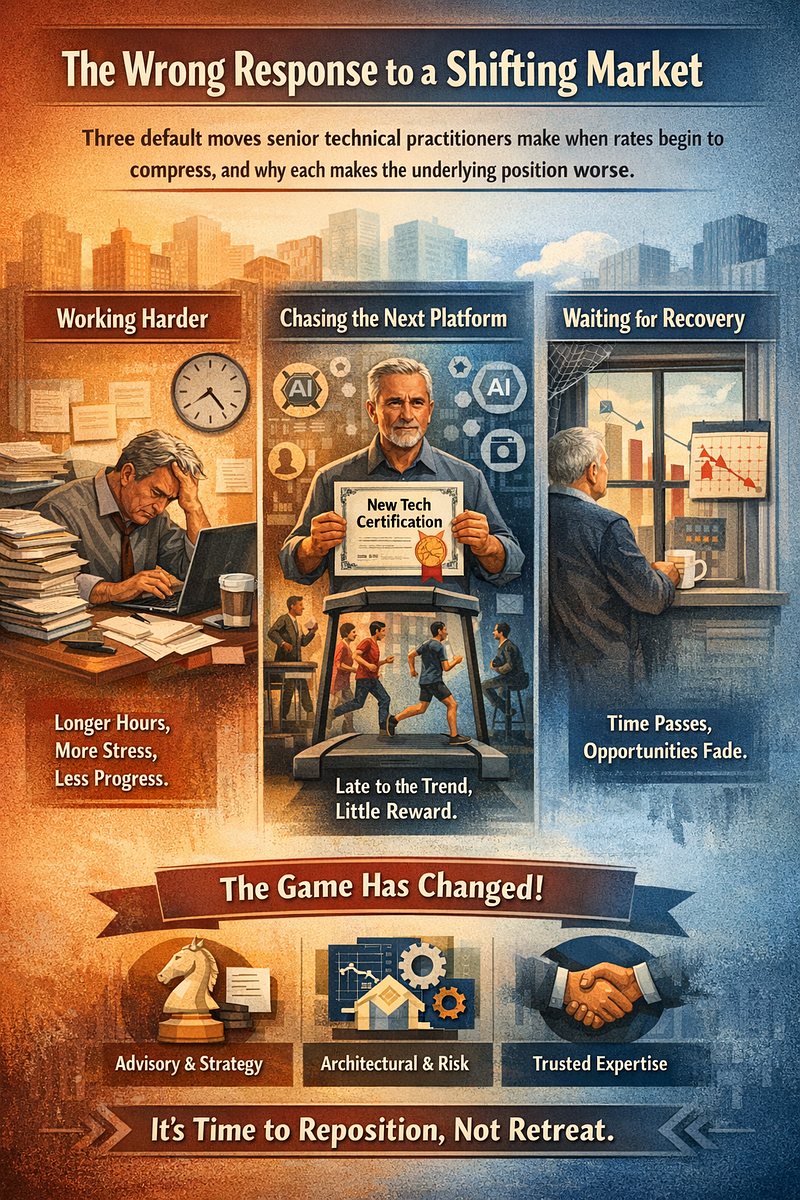

The Wrong Response to a Shifting Market

Three default moves senior technical practitioners make when rates begin to compress, and why each makes the underlying position worse.

Three default moves senior technical practitioners make when rates begin to compress, and why each makes the underlying position worse.

A familiar pattern is visible among senior technical practitioners. The market for their services has begun to shift. Rates are softer than they were three years ago. Engagements are shorter. Junior teams, augmented by AI tooling, are producing work at speeds that would have been implausible in 2022. The senior practitioner responds. Usually in one of three ways.

The practitioner often feels the shift before naming it. The rate resistance at the last contract negotiation. The client who asked what AI could do for their project. The dinner conversation where a younger colleague described delivering in two weeks what used to take two months. The referral that did not come this quarter. These details accumulate into a background disquiet that sits behind the calendar and the client calls, and that is usually not spoken of with anyone — not with colleagues, who are competitors, and not with clients, to whom the disquiet cannot be shown.

The first response is to work harder. More hours, more projects, a tighter schedule, perhaps a second engagement running in parallel with the first. The second is to learn the newest platform — to certify in whatever the current fashion is, whether Databricks, Snowflake, or one of the AI-adjacent specialties — on the assumption that additional technical breadth will restore the lost pricing power. The third is to wait: to assume that the current market conditions are a temporary distortion and that rates will recover once the AI hype cycle settles and enterprises remember the value of experience.

All three responses are wrong. In most cases, they make the underlying position worse.

What they have in common is more important than what distinguishes them. Each of the three assumes that the game being played has not changed, only that the difficulty has increased. Work harder at the same game. Certify for the same game. Wait out a bad patch of the same game. The evidence is against this. The game has changed. The pricing structure of senior technical implementation work is being reset, not temporarily suppressed. Competing harder, credentialing more, or waiting longer within the old structure produces worse outcomes than repositioning outside of it.

Working Harder

The instinct to work harder is the most natural response. It is also the most costly. It is natural because every senior practitioner has built their career on exactly this response. Harder work solved earlier problems — the tight deadline, the difficult client, the underperforming colleague, the technology transition. The assumption that it will solve this one as well is defensible on past evidence. It is also wrong.

The exhaustion has a different character at fifty-five than it had at forty. It is physical, not emotional. A Saturday does not restore it. The body registers cumulative load differently than it did twenty years earlier, and the practitioner notices this, usually in private, and usually without mentioning it. To mention it would be to admit that the terms of trade have shifted. Most practitioners are not yet ready to admit that, even to themselves.

The problem with working harder in the current market is not that it fails to produce results. It produces results. Each additional engagement billed, each weekend worked, each parallel project delivered translates into revenue. The problem is that each unit of effort produces less revenue than it did three years ago, and the trajectory is downward rather than flat. Working harder at a rate that is being compressed means earning more hours of labor but less per hour. The additional hours do not compensate for the lower rate.

There is a second problem, which matters more than the revenue question. Working harder consumes the exact resource that would make repositioning possible. Repositioning — the development of a different service, a different pricing structure, a different market position — requires time to think, to write, to build relationships, to design offerings that do not yet exist. A practitioner working sixty-hour weeks at the existing practice has no such time. The harder they work at the current model, the less capacity they have to construct the next one.

Consider a pattern. A senior freelance consultant in European banking, with twenty years of experience as an Informatica specialist, charged his peak rate in 2022 for roughly 150 billable days a year. By 2025, under rate pressure and with shorter engagements, he accepts roughly 20 percent less per day but bills 40 percent more days across parallel projects. His gross revenue is roughly flat. His exhaustion is higher. His rate trajectory is still downward. Over three years, he has produced no publications, no specialized offerings, no partnerships — no assets that would allow him to reposition when the current rate compresses below the level at which additional days can compensate.

The cost compounds. A senior practitioner who spends three years working harder at an eroding rate has, at the end of those three years, lower rates, depleted energy, no new assets, and no repositioning in progress. A practitioner who spent the same three years working somewhat less but building a differentiated position has, at the end, a practice that commands what the old one did or more. The first path looks prudent year by year. The second looks prudent only when the full arc is visible. Most practitioners do not see the arc until the third or fourth year. By then, the gap between the two paths has become difficult to close, and the recognition itself is painful in a specific way — the pain of having worked very hard on something that was worsening the situation.

Learning the Newest Platform

The second response is more sophisticated but fails in a different way. Certifying on the current platform of record — Databricks today, whatever the market favors eighteen months from now — feels like the exact kind of professional development that the situation demands. The reasoning is straightforward. Rates are compressing in the old specialty. The new specialty is where the budget is moving. Credentialing in the new specialty should therefore restore the lost pricing.

This reasoning is wrong in three ways.

The first is that certification lags market demand by 12 to 18 months, meaning that by the time a senior practitioner completes the certificate on the current platform of interest, junior practitioners have already accumulated meaningful project experience in it and are being priced accordingly. The certificate does not close that gap. It credentials a position that younger competitors already occupy with both certification and experience. The senior practitioner arrives at the new platform as a late entrant, without the cost advantage that typically allows late entrants to compete.

The second is that the premium historically paid for deep expertise is not being paid, in the current market, for deep expertise in the newest platform. It is being paid for deep expertise in legacy systems that regulated industries are still running and cannot easily replace. A practitioner with twenty years of enterprise data warehousing experience is paid a premium for that experience because banks and insurers cannot easily source it. A practitioner who has recently certified on Databricks is paid roughly what any Databricks-certified consultant is paid, with general seniority adjusted modestly upward. The premium attaches to scarce expertise, not to fashionable expertise.

The third is that the treadmill does not stop. A practitioner who certifies on the current platform this year will need to certify on the next one in two years, and the one after that in four. Each certification cycle consumes months of effort that do not produce revenue, and the underlying pricing structure of whatever the current platform is continues to compress as AI tooling reaches it. The treadmill is not a path to a better position. It is a mechanism for preserving the current position at increasing cost, and for most practitioners, it ends in exhaustion rather than in repositioning.

There is a further cost, less visible in the accounting. The senior practitioner who certifies on a new platform is, within that platform's social structure, a junior. They sit in courses next to practitioners half their age. They answer certification exam questions about concepts they have encountered for 6 months, while colleagues around them have worked with those same concepts for 3 years. The asymmetry is not cruel — it is simply the fact that the platform is new and they are new to it. But the experience does something to a practitioner who has spent two decades being the person consulted rather than the person learning. No amount of framing it as humility removes what the body registers. Something has been relinquished that was not relinquished voluntarily.

Consider the practitioner who acts on this reasoning. A senior Oracle DBA with eighteen years in Austrian insurance, observing that Oracle engagements are shortening, completes a Databricks certification in 2024 at a cost of six months of part-time study. He expects rates comparable to his legacy Oracle work. His first Databricks engagement in 2025 pays roughly 35 percent less than his previous Oracle rate, which is the going rate for newly certified Databricks consultants regardless of seniority. His 18 years of Oracle experience are seen by the market as irrelevant to the new role. His prior specialty — still in demand at banks and insurers running legacy systems — has been de-emphasized during the transition. Reclaiming it now would require rebuilding relationships he allowed to lapse.

None of this argues against learning new platforms. It argues against treating certification as the repositioning itself. Platform competence is necessary to remain credible in the market. It is not sufficient to command premium pricing, and treating it as sufficient is the error.

Waiting for the Market to Correct

The third response is the quietest and, in some ways, the most damaging. It consists of continuing the existing practice substantially unchanged, reducing rates modestly when necessary to retain engagements, and assuming that the current market conditions are a temporary distortion produced by AI hype that will normalize within a reasonable period. The premise is that experience will reassert its value once the current enthusiasm for AI-augmented junior teams meets the reality of what those teams can actually deliver in regulated enterprise environments.

The premise contains some truth, which is why it is seductive. AI tooling in 2026 is producing work of uneven quality at enterprise scale, and a correction will occur as organizations discover the limits of the current approach. The expected correction, however, is not a return to the previous market structure. It is a reshaping of the market into a structure in which AI-augmented teams remain central and senior practitioners are absorbed into different roles within that structure — architecture, governance, advisory, exception handling — rather than restored to the implementation work they previously occupied.

Waiting, therefore, is not a neutral posture. It is a bet that the market will return to its previous state. That bet is unlikely to pay out, and while it is not paying out, the practitioner who has made it is burning through reputational capital and cash reserves in a practice that is slowly contracting. The patient strategy becomes, over time, a liquidation strategy.

The waiting produces a specific kind of loneliness. Colleagues who repositioned are too busy with their new practices to describe how they did it. Colleagues who did not will not say aloud that they did not. Spouses may sense that something is wrong, but usually do not know the specifics of day rates or engagement structures well enough to help. The practitioner carries the situation alone, often for years, while the external evidence accumulates quietly — the referral that did not come, the renewal that was not offered, the invitation to the advisory board that went to someone younger. None of these events, taken individually, is a crisis. Taken together, they describe a trajectory. The practitioner recognizes the trajectory before anyone around them does, and usually before they are ready to act on the recognition.

Consider the practitioner who takes this path. A senior data warehouse architect with 22 years of experience across European banking and telecom, respected in his sector, chose in 2022 to maintain his practice unchanged on the assumption that rates would recover. Between 2022 and 2025, his day rate declined by roughly 30 percent through a series of individually reasonable concessions to retain clients. Engagements grew shorter. Referrals slowed as his peers repositioned into adjacent areas where he did not appear. By 2025, his reputation was intact, but his practice had contracted significantly. He had produced no new assets — no book, no partnerships, no differentiated offerings — that would allow him to move now from a weaker starting position than he held three years earlier. The three years of waiting did not preserve his position. They eroded it slowly enough that no single year’s erosion felt serious, until the cumulative effect became visible.

The asymmetry is clear. Waiting has a low ceiling and a substantial floor risk. Repositioning has a higher ceiling and a comparable floor risk. The expected value of waiting is almost certainly lower than that of repositioning, and the distribution is worse on the downside as well.

The Common Error

Each of the three responses shares a hidden premise. The premise is that the market is the same market it was three years ago, only more difficult, and that the correct response is to compete harder, credential more, or wait patiently within the existing structure. The premise is false.

The market has not become more difficult. It has become different. Implementation work at the senior level — the work of building, tuning, and delivering data platforms or equivalent enterprise technology — is being systematically repriced downward because AI tooling is compressing the time required to produce it. This is not a temporary distortion. It is a structural shift in the underlying economics, and it is likely to continue and intensify over the next several years rather than reverse.

What is not being repriced downward, or at least not to the same degree, is a different kind of work. Architectural judgment about which systems to build and why. Advisory work on regulatory obligations, risk frameworks, and the interaction between business strategy and technical constraints. Design work at the boundary between business domains and technical implementation, where the translation requires deep experience in both. Trust-based relationships with senior stakeholders who rely on the practitioner for judgment rather than for hours. These categories of work are harder to compress with AI tooling because they depend on context, relationships, and tacit knowledge that no tool can produce.

The senior practitioner whose revenue is primarily from implementation is competing in the compressed market. The senior practitioner whose revenue is primarily advisory, architectural, or judgment-based is competing in a stable or growing market. The correct response to the current shift is not to work harder at implementation, not to certify in new implementation platforms, and not to wait for implementation rates to recover. It is to shift the practice's center of gravity away from implementation and toward the categories of work that are not being compressed.

This is a slower response than any of the three wrong responses. It requires changing what the practice sells, not just how much is sold or at what price. Most practitioners resist this because the existing offering is familiar and the new one is not, because the transition itself creates revenue uncertainty, and because the work of repositioning is qualitatively different from the work they have been doing for 20 years.

The resistance has another source, which is worth naming even if dwelling on it would not help. A practice built over twenty or twenty-five years is not only a source of income. It is a structure of identity. The specific technologies, client relationships, reputation, and way of introducing oneself at industry events — these are not interchangeable parts that can be swapped out when market conditions change. They are what the practitioner became over the course of their adult working life. Asking a senior practitioner to reposition is not asking them to change jobs. It is asking them to become a different professional self while continuing to support whatever dependents, obligations, and plans were built on the existing self. The difficulty of this is not an excuse. But pretending it is not difficult is the reason so much advice on this topic fails to reach the people it claims to be for.

The Direction of a Correct Response

The full shape of a correct response is beyond the scope of a single essay and will be developed at length in subsequent work. The direction, however, can be stated in general terms.

A correct response begins not with activity but with diagnosis. Before new services are built, new pricing structures are designed, or new market positions are pursued, the practitioner should conduct an honest assessment of what the existing practice actually sells, to whom, and on what basis. The assessment is uncomfortable because it often reveals that the practice is selling implementation hours to buyers who do not distinguish between senior and junior implementation, which is the position from which rates compress fastest.

The uncomfortable part is not the logical recognition. It is what happens when a practitioner, alone with a spreadsheet or a list of past engagements, reaches the conclusion that the answer to “why would a client still pay premium rates for this” is thinner than they had been telling themselves. There is usually a moment in the diagnosis when what had been suspected becomes undeniable. The moment is unpleasant. It is also the moment from which every subsequent good decision follows.

The diagnosis is followed by a decision about where in the value chain the practice should operate. The options are not infinite. Most senior technical practitioners, for structural reasons, will find that the correct position is somewhere in the territory bounded by architecture, advisory, specialized design, and trust-based long-term advisory relationships with enterprise clients. The position depends on the practitioner’s credentials, relationships, and areas of deepest expertise. It is not a matter of choosing freely from a menu but of identifying which of the limited number of viable positions the practitioner is best credentialed to occupy.

Once the target position is identified, the repositioning consists of three parallel efforts. The first is the construction of offerings that serve that position, which usually means retainer-based advisory, fixed-fee architecture engagements, or specialized consulting packages rather than hourly implementation. The second is the development of assets that establish credibility in the new position — publications, partnerships, case studies, and credentials that signal to buyers that the practitioner operates at the advisory rather than implementation level. The third is the gradual migration of existing clients toward engagements that fit the new position, and the selective acquisition of new clients who arrive already seeking the advisory work rather than the implementation work.

Three worked examples illustrate what this looks like in practice.

The first is a senior IBM DataStage consultant in European banking who, in 2024, stopped accepting any implementation engagements. She restructured her offering around fixed-fee architecture reviews for bank-wide data platform migrations, priced at a premium that reflects the architectural value rather than the implementation time. She now runs four of these per year, supplemented by two advisory retainers. Her gross revenue is roughly 15 percent higher than in 2022. Her effort is lower. She no longer competes on day rates against AI-augmented junior teams, because her offering is not priced in days. The move required her to turn down implementation engagements for nine months while the new offering established itself. The period felt costly at the time. In retrospect, it was the narrow window in which the repositioning was even possible.

The second is a senior SAP consultant at an Austrian insurance company who repositioned as a regulatory advisory specialist for finance compliance. Rather than billing implementation hours, he now runs multi-year advisory retainers with a small number of clients. His implementation work has declined to near zero, and he considers that an improvement rather than a loss. The advisory retainer format makes him nearly immune to AI-driven price compression because the value he provides is regulatory interpretation and risk judgment — work that depends on his twenty years of observed regulatory behavior across European financial institutions and that no tool can produce. His gross income is roughly 20 percent higher than at his peak billable-hour practice in 2021, from approximately 40 percent fewer working hours.

The third is a senior data warehouse architect in DACH telecom who invested eighteen months in writing a book on enterprise migration strategy. The book did not earn meaningful royalties and was never intended to. It anchored his credibility as an authority on migration architecture. That credibility allowed him to reposition from hourly implementation to fixed-fee engagements at the strategy level, where his twenty-five years of experience finally commanded a premium that reflects their actual value rather than a premium compressed by commoditization in implementation work. His total billed days per year declined by 40 percent between 2022 and 2025. His gross income rose by 30 percent over the same period. The time freed by fewer billable days is being invested in a second book and a conference speaking program that he expects will drive the next stage of premium pricing.

The three examples illustrate different forms of the same move: changing the pricing structure from days to a fixed fee, changing the service from implementation to advisory, and using content assets to anchor premium pricing for work that is substantively similar to what was sold before. None of the three practitioners learned a new platform as the primary repositioning move. None worked harder than they had been working. None waited for the market to recover. Each constructed a position that the compressed implementation market does not reach.

None of this is fast. The repositioning timeline for most practitioners is 2 to 3 years, not 2 to 3 months. The practitioner who begins the work in year one is substantially repositioned by year three. The practitioner who begins in year three is starting the repositioning work from a weaker financial and reputational position than they would have had in year one, and the process is correspondingly harder.

What to Do This Quarter

The most useful question a senior technical practitioner can ask this quarter is not “what new skill should I learn,” or “which platform should I certify on,” or “when will the market recover.” It is a different question. What position should this practice occupy, and what would have to be true for it to occupy that position in three years?

Answering that question well is the beginning of the correct response. The answer, when it is honest, will usually reveal that the practice is not currently positioned where it needs to be in three years, and that deliberate reconstruction is required. The reconstruction is the work. Working harder at the existing position, certifying on a new platform, or waiting for a correction are substitutes for the work. They feel productive because they are familiar and because they produce visible activity. They are not productive. The work — the diagnosis, the repositioning, the gradual reconstruction of what the practice sells and to whom — is what produces durable outcomes in a market that will not return to what it was.

The senior technical practitioner who begins this work in 2026 will be substantially repositioned by 2028. The practitioner who defaults to one of the three wrong responses will, in 2028, be in a materially worse position than today. The market will not return to its previous structure. The practitioners who act on that premise, now, will find that senior expertise still commands premium rates — in a market they have deliberately constructed rather than one they have waited to be restored.

One more observation. The practitioners who are currently navigating this, often alone and usually without speaking to anyone about it, are not few. The specific experience of being a senior technical expert between forty-five and sixty in the current market — watching a practice built across two decades or more shift under conditions that were not foreseen and cannot be easily reversed — is not an individual failing. It is a demographic condition. It is happening to a large population at once, across several countries and specialties, at the same time. Recognizing that it is shared is not a solution. But the isolation in which the situation is usually faced makes it harder to see clearly than it needs to be, and makes the first necessary step — the honest diagnosis — harder to begin. The first step is the diagnosis. The second, nearly as useful, is the recognition that the diagnosis does not belong solely to the practitioner.

The examples in this essay are composites drawn from patterns observed across European enterprise consulting. They illustrate repositioning patterns but do not describe specific individuals.